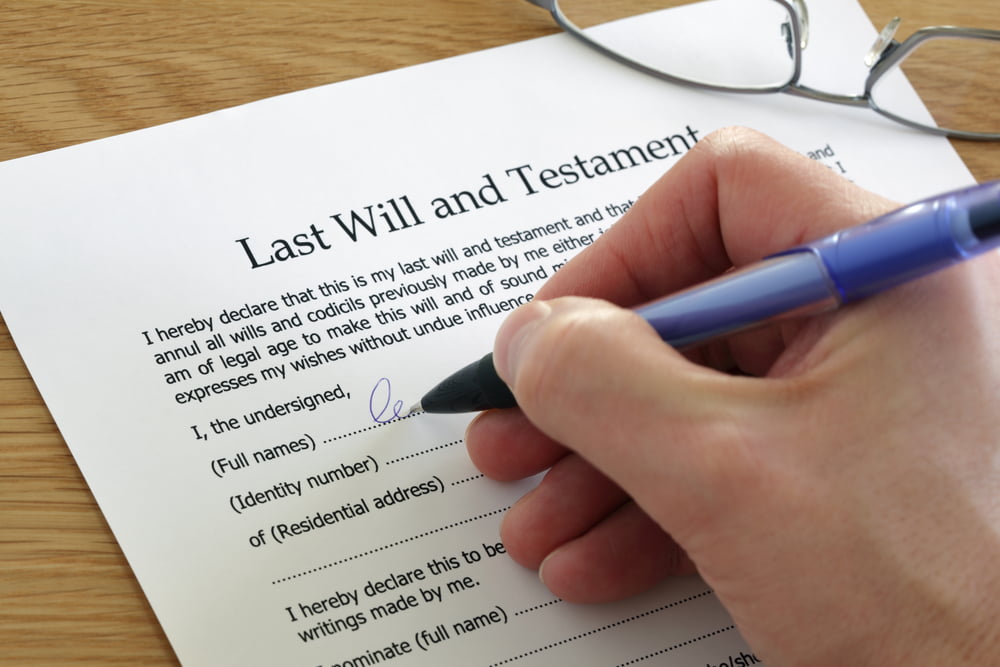

It’s important to make a will or update one so that your assets are distributed in the way you would like, but it’s also essential to protect your children. Regardless of your personal situation, you should always have an up to date will…

Making a will or updating one is a morbid topic, and many of us are often tempted to put it off. Understandably, we don’t like to think about our own mortality. Research published in 2018 from insurer Royal London revealed that 54 per cent of UK adults did not have a will and 5.4 million had no idea how to make one.

The pandemic has fortunately encouraged more people to address this. The number of people enquiring about making a will has risen by a whopping 267 per cent in the last 12 months. It seems we are now starting to think more carefully about what we would like to happen to our assets when we die.

More younger people making wills

Interestingly, the biggest rise in those enquiring about a will has been among the under 35s, with a 300 per cent increase. This is good news, as making a will is not just a task that sick or elderly people should do. Everyone adult should make a will and it’s not just about ensuring that your assets go where you’d like them to after you die.

Making a will with clear instructions about your intentions will save your family a considerable amount of stress during a difficult time.

If you die without making a will, your family may need to obtain legal advice and complete extra paperwork in addition to coming to terms with their loss. They will also have no idea what your intentions are as to whether you’d like to be cremated or buried, which can be very upsetting.

Protect your children

In addition, if you die without appointing a legal guardian for your children (which you can only do in your will) the family courts will decide where your children will live and in the meantime, they will be placed into care. This process can take months to resolve.

So as you can see, making a will is not just about where you want your money to go after you die. However, the financial aspect is also an important consideration for many. If you pass away without making a will, your assets will be shared out according to what’s known as the rules of intestacy. Only married and civil partners (and some other close relatives) can inherit under these rules.

Your personal belongings

If you are married or in a civil partnership at the time of your death, and you have children, grandchildren or great grandchildren, your spouse will inherit all of your personal property and belongings, plus the first £270,000 of your estate, and half of your remaining estate. If there are no surviving children, grandchildren or great grandchildren, they will inherit all of your personal property and belongings and all of your estate.

It’s important to think clearly about what you would want to happen in the event of your death. You may want your children or grandchildren to inherit some of your personal belongings, such as an item of jewellery. However, if you die without making a will, all of your personal belongings will go to your spouse.

If you live with a long-term partner but you’re not married or in a civil partnership (i.e. you’re simply cohabiting) and you die without making a will, they can’t inherit under the rules of intestacy. Unmarried partners or partners who have not registered a civil partnership will not inherit from each other unless they have made a will.

If you die without making a will and you live with your partner, they may not inherit the property depending on how you jointly own the property.

Owning a property

There are two different ways of owning a property jointly. One way is as beneficial joint tenants and the other is as tenants in common. If you are beneficial joint tenants at the time of death, the surviving partner will automatically inherit the other person’s share of the property. You may not want this to happen. However, if you are tenants in common, the surviving partner does not automatically inherit your share. The best way to ensure your assets are distributed in the way in which you would like is to make a will.

You might also want to think about organising Lasting Power of Attorney (also known as LPA). There are two types, Property & Financial Affairs and Health & Welfare. An LPA is a legal document that lets you appoint one or more people to make decisions on your behalf if you are unable to do so.

Lasting Power of Attorney

Property & Financial Affairs LPA enables the person to make decisions about your banking, paying of bills, collecting benefits or a pension or selling your home.

Health & Welfare includes decisions relating to your medical care, moving into a care home or having life-sustaining treatment.

If you were involved in an accident, or if you were to lose mental capacity due to an illness such as a form of dementia, Lasting Power of Attorney would therefore mean that someone else would be able to make decisions for you. We recommend having both types of Lasting Power of Attorney.

More information

At MB Associates, we work with trusted partners and can help you with the process of making a will or Lasting Power of Attorney. Feel free to get in touch with us for more information.